Kenya Real Estate Finance Bill 2025

Why Kenya Needs a Real Estate Finance Reform Bill

Kenya’s property sector is starved of long-term, affordable financing. Despite a massive housing deficit (estimated at 2 million units), only ~30,000 mortgages are active nationwide — due to:

- High interest rates (13–16% average)

- Stringent collateral requirements

- Low public awareness of alternative financing

- Fragmented regulation across CBK, CMA, Ministry of Lands, and NHC

A coordinated “Real Estate Finance Bill” could align laws, unlock capital, and make homeownership achievable for millions.

🔮 7 Likely Components of a Future Kenya Real Estate Finance Bill

1. Mortgage Interest Rate Cap or Subsidy Scheme

“The Bill may cap mortgage rates at 10% for affordable housing units or introduce government interest subsidies.”

- Modeled after programs in Egypt, India, and South Africa

- Could apply to homes under Ksh 5 million (aligned with Affordable Housing Programme)

- Funded via National Housing Fund or Treasury guarantees

2. Mandatory Employer Housing Contributions (Like NHIF/NSSF)

“Employees may contribute 1–1.5% of salary to a National Housing Development Fund — matched by employers.”

- Similar to Singapore’s CPF or Malaysia’s EPF

- Funds could be used for down payments, mortgage top-ups, or retirement housing

- Managed by NHIF or a new Housing Finance Authority

3. Tax Incentives for Developers & REITs

“Developers of affordable housing may receive 10-year tax holidays, VAT exemptions, or reduced stamp duty.”

- Encourage private sector participation in Big 4 projects

- Boost REIT formation by reducing capital gains tax on property transfers into trusts

- Allow 100% mortgage interest deduction for first-time buyers (currently limited)

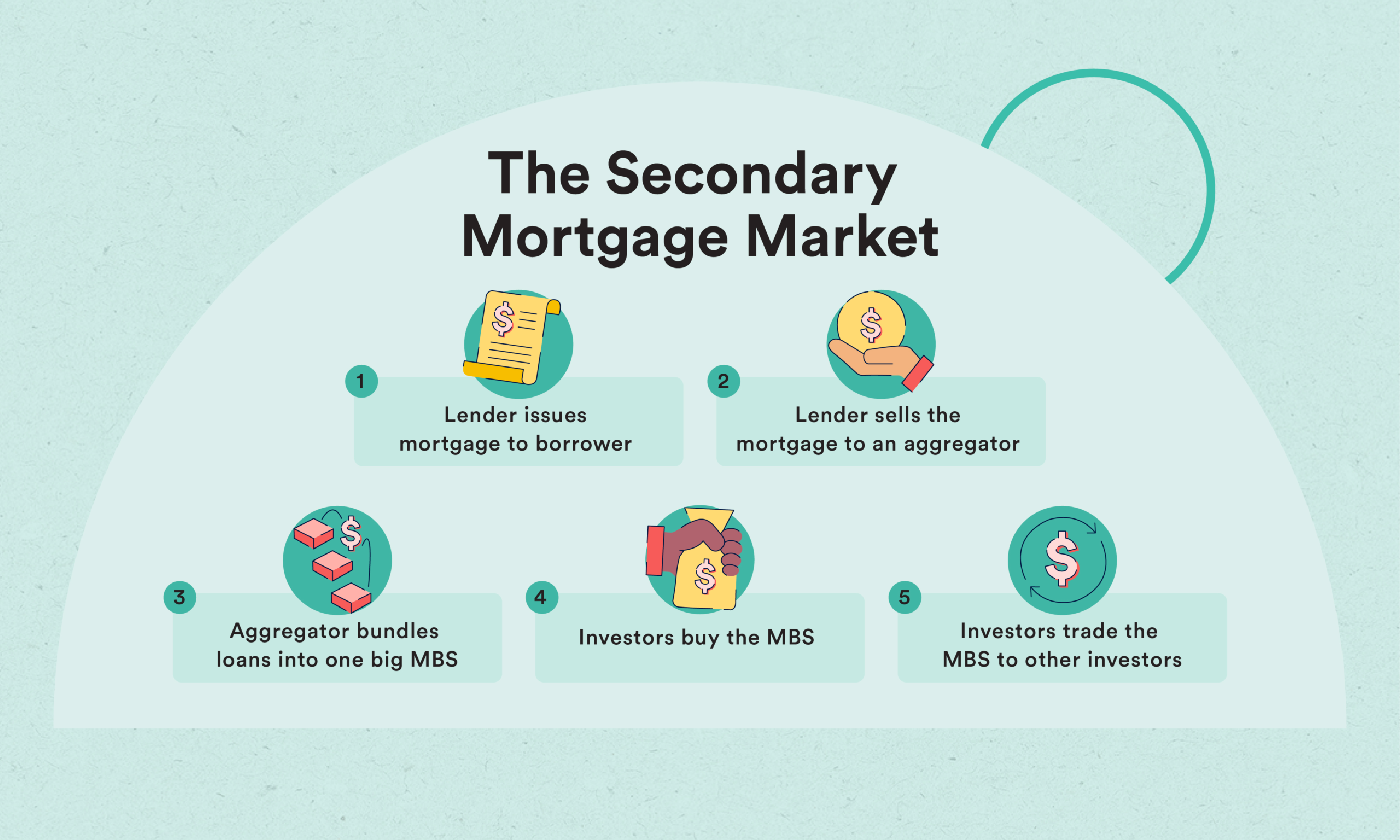

4. Establishment of a Secondary Mortgage Market

“Banks may be allowed to package and sell mortgages to institutional investors — freeing up capital for new loans.”

- Modeled after U.S. Fannie Mae / Freddie Mac

- Backed by a government guarantee agency to reduce investor risk

- Could dramatically increase mortgage availability

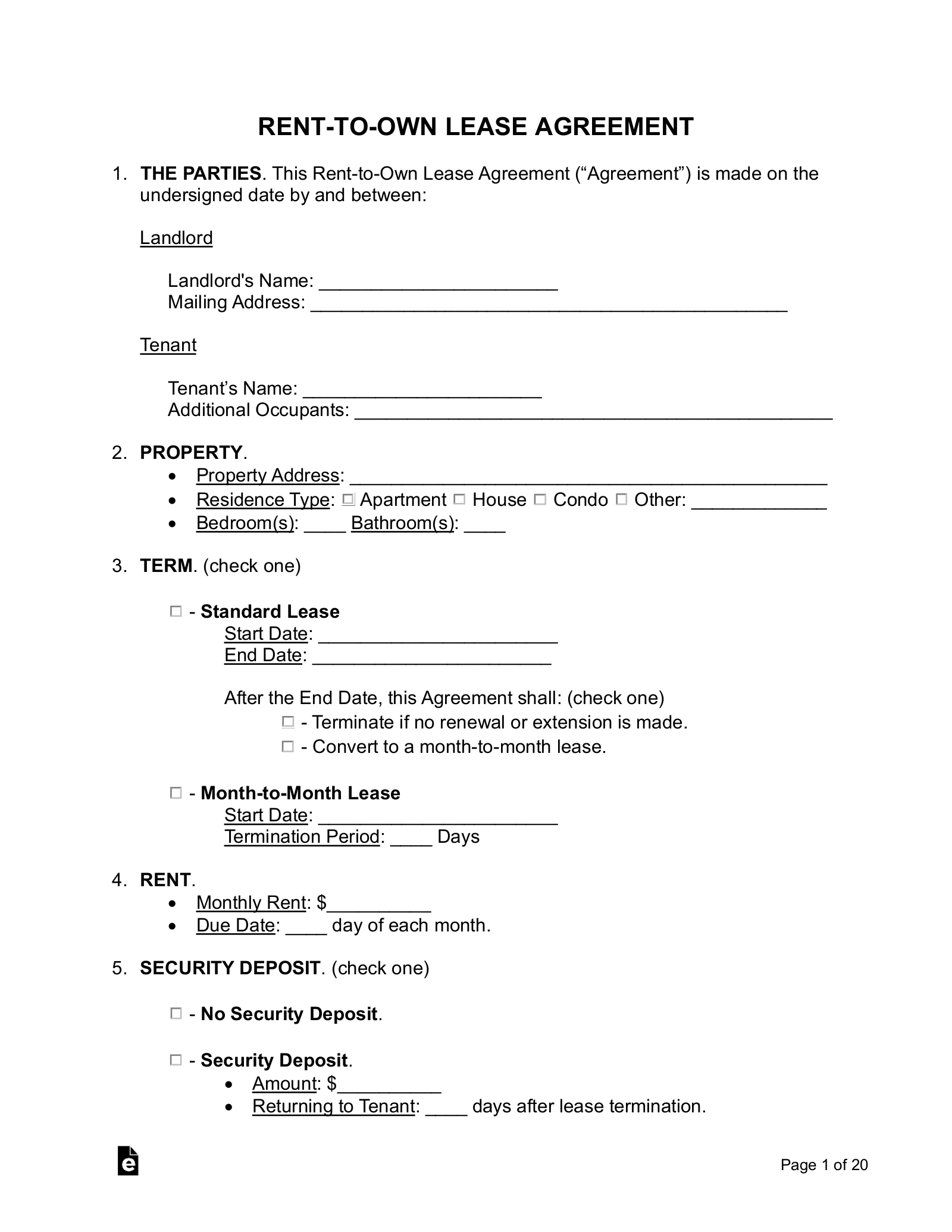

5. Rent-to-Own Legal Framework

“Formalize and regulate rent-to-own schemes — protecting tenants and enabling gradual ownership.”

- Requires standardized contracts, escrow accounts, and title transfer timelines

- Prevents exploitation by unregulated developers

- Supported by Ministry of Lands and CMA

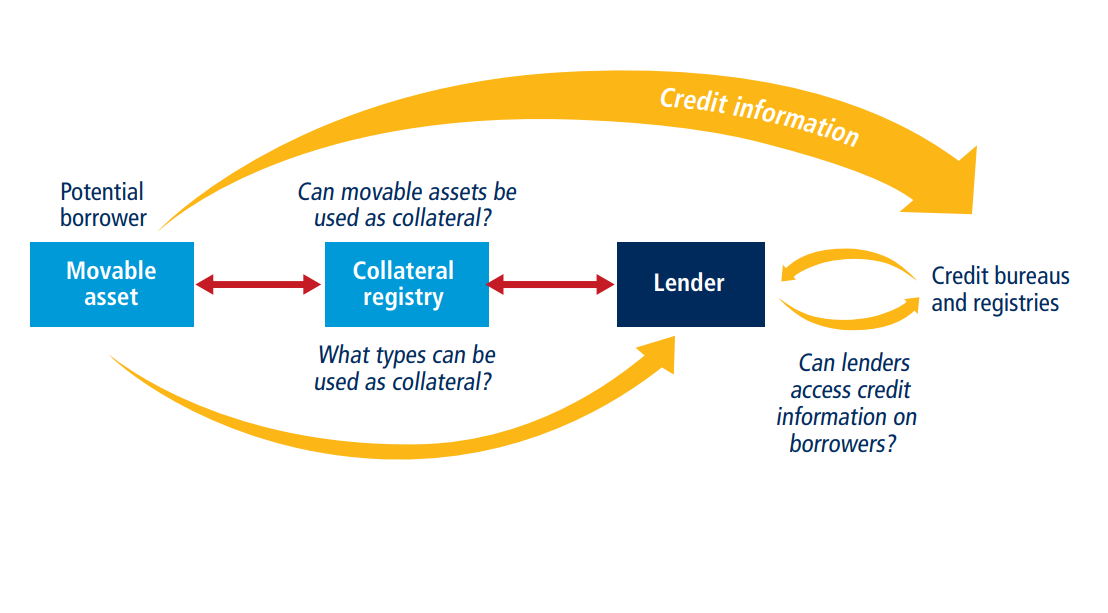

6. Digital Mortgage Registry & Collateral Registry Integration

“All mortgages to be registered digitally via e-Citizen — integrated with CRB and Lands Registry.”

- Reduce fraud and double-pledging of property

- Speed up loan processing (target: 14 days from application to disbursement)

- Enable “mobile mortgages” via fintech partnerships

7. Inclusion of Diaspora & Informal Sector Workers

“Diaspora Kenyans and informal workers may access mortgages using alternative credit scoring (mobile money, SACCO records).”

- Partner with World Bank, IFC, and fintechs like Tala, Branch, or Pezesha

- Accept remittance history as income proof

- Link to Huduma Namba and e-Citizen for KYC

🏗️ Current Laws & Policies That May Feed Into This Bill

While no “2025 Bill” exists yet, these active frameworks may evolve into it:

| Affordable Housing Act (2023) | Provides legal basis for housing projects, contributions, and allocations. |

| Finance Act 2024 | Introduced 3% housing levy (now suspended) — may be redesigned. |

| CBK Prudential Guidelines | Encourage banks to increase mortgage lending with better risk models. |

| CMA REIT Regulations (2013) | May be amended to incentivize more REITs as financing vehicles. |

| National Housing Corporation (NHC) Strategy | Pushing for blended finance models and public-private partnerships. |

⚠️ Note: The 3% Housing Levy was halted by the High Court in 2023. Any new bill must address this legally.

💡 Who’s Advocating for Real Estate Finance Reform?

- Central Bank of Kenya (CBK) → Pushing for deeper mortgage markets

- Capital Markets Authority (CMA) → Promoting REITs and securitization

- Ministry of Lands & Housing → Driving Affordable Housing Agenda

- Kenya Bankers Association (KBA) → Lobbying for risk-sharing facilities

- Private Developers (Home Afrika, Acorn, etc.) → Seeking tax breaks and faster approvals

- Civil Society (Haki Jamii, Kituo cha Sheria) → Demanding inclusive, transparent frameworks

❓ Frequently Asked Questions (FAQs)

Q: Is the Kenya Real Estate Finance Bill 2025 law yet?

A: No. As of April 2025, no such bill has been introduced in Parliament. This is a speculative analysis based on policy trends.

Q: What happened to the 3% housing levy?

A: It was suspended by the High Court in 2023 following public petitions. Any new financing model must pass constitutional muster.

Q: How can I access affordable financing now?

A: Try:

- NHIF Affordable Housing Scheme (if you’re a contributor)

- Banks: KCB MyHome, Co-op Bank Home Loan, Stanbic Ibtc

- SACCOs: Stima, Afya, Harambee

- Developers: Home Afrika, Bryan Properties (installment plans)

Q: Will this bill lower mortgage rates?

A: Potentially — through subsidies, risk-sharing, or interest caps. But banks’ cost of funds must also decrease.

Q: How can I stay updated?

A: Follow:

- Parliament of Kenya Bills

- Ministry of Lands & Physical Planning

- CBK Financial Stability Reports

- News outlets: Business Daily, The Standard, NTV Kenya